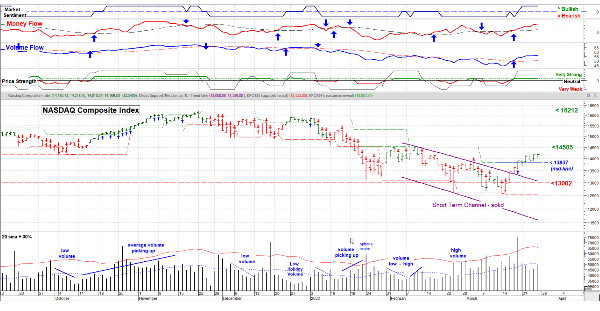

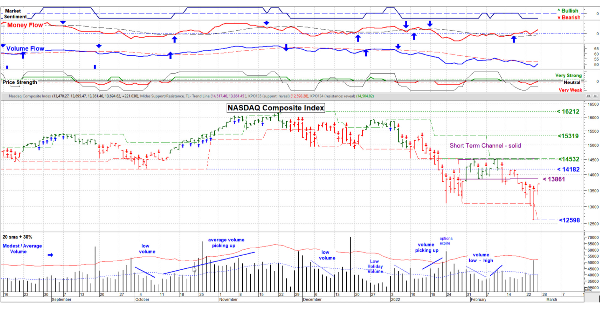

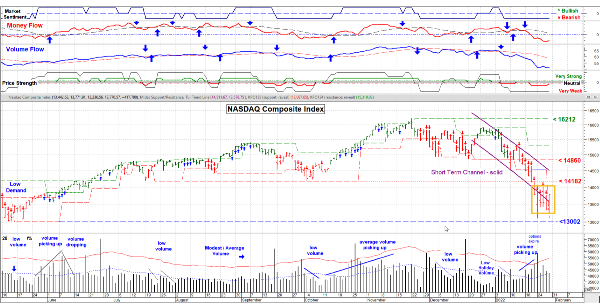

March 25, 2020 – A good week for the markets. Up past my “mid-line” and every indicator on the chart below is positive / bullish. But . . . Ukraine still holds over the market, as does inflation and “fear” of interest rates rising. The market seems to say “OK, I’m feeling better, but not entirely well”. Note the rather low volume, below the 20 day average . . . no rushing to jump back in by institutions.

The big factor will be the upcoming corporate earnings reports. If the majority can show modest growth then I think we’ll be “off to the races”, or at least firmly toward new highs. How profitable companies are in this environment really says it all since skepticism abounds in the long term. But employment is at an all-time high, interest rates are very low by historic measure and inflation was expected coming off the COVID lock downs. Oh yes, COVID could be a wild card in the entire scheme of things.

So what to expect? In short, the unexpected. The war . . . who knows what Putin will do. COVID . . . we’re in much better shape to deal with it now. Inflation . . . slowly getting under control late in the year as supply chains improve. Corporate earnings . . . pretty darn good, except for some pockets of poor. I’m thinking that the next 2-5 years will be a stock / industry sector pickers market; everything will not be going higher at the same rate, nor at the same time. Those days are behind us (I think).

How to handle this is via a “Top Down” analysis approach. Starting with market health, then sector strength, then industry strength and lastly stocks in those industries. More on this later.

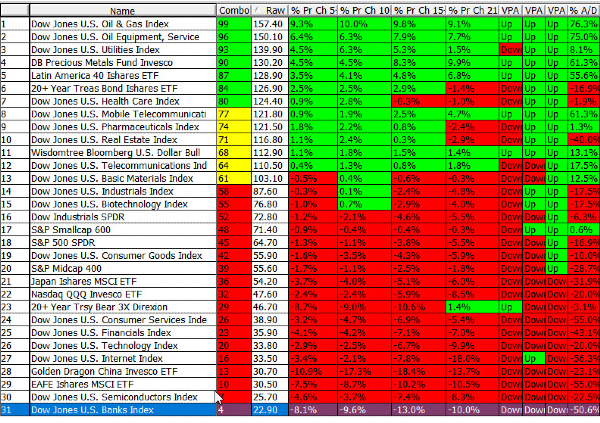

for more discussion & Sector Strength table: www.special-risk.net

chart by MetaStock, used with permission

I/we have a position in an asset mentioned

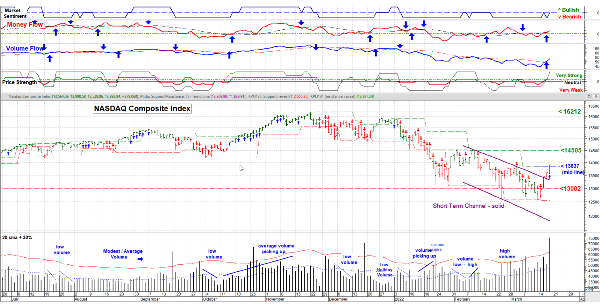

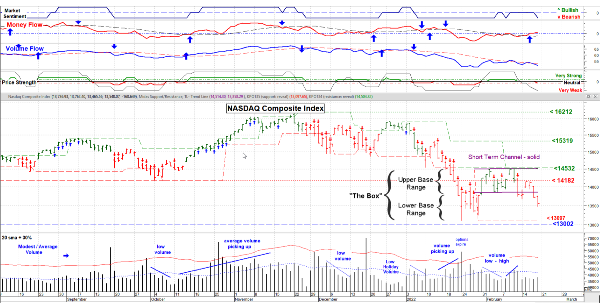

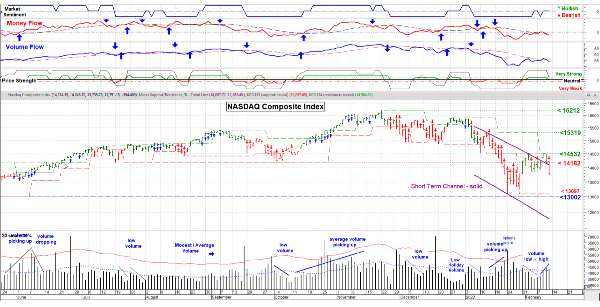

March 25, 2020 – A good week for the markets. Up past my “mid-line” and every indicator on the chart below is positive / bullish. But . . . Ukraine still holds over the market, as does inflation and “fear” of interest rates rising. The market seems to say “OK, I’m feeling better, but not entirely well”. Note the rather low volume, below the 20 day average . . . no rushing to jump back in by institutions.

The big factor will be the upcoming corporate earnings reports. If the majority can show modest growth then I think we’ll be “off to the races”, or at least firmly toward new highs. How profitable companies are in this environment really says it all since skepticism abounds in the long term. But employment is at an all-time high, interest rates are very low by historic measure and inflation was expected coming off the COVID lock downs. Oh yes, COVID could be a wild card in the entire scheme of things.

So what to expect? In short, the unexpected. The war . . . who knows what Putin will do. COVID . . . we’re in much better shape to deal with it now. Inflation . . . slowly getting under control late in the year as supply chains improve. Corporate earnings . . . pretty darn good, except for some pockets of poor. I’m thinking that the next 2-5 years will be a stock / industry sector pickers market; everything will not be going higher at the same rate, nor at the same time. Those days are behind us (I think).

How to handle this is via a “Top Down” analysis approach. Starting with market health, then sector strength, then industry strength and lastly stocks in those industries. More on this later.

for more discussion & Sector Strength table: www.special-risk.net chart by MetaStock, used with permission

I/we have a position in an asset mentioned